As Bitcoin Soars, Nigerians Face Central Bank Crackdown

Nigeria, a nation with one of the highest cryptocurrency adoption rates globally, is experiencing a surge in Bitcoin use amidst a backdrop of tightening foreign exchange (FX) controls. This has led to a tense relationship between the Central Bank of Nigeria (CBN) and the country’s burgeoning crypto community.

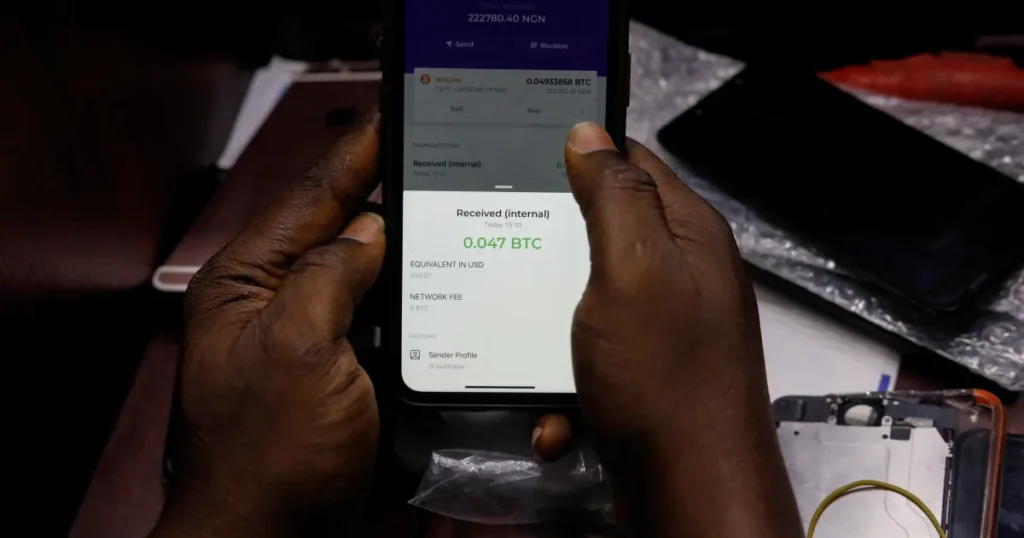

Bitcoin prices have skyrocketed in recent weeks, surpassing the $71,000 mark. This surge has enticed many Nigerians, who view cryptocurrency as a hedge against inflation and a potential path to financial security. The Nigerian Naira, on the other hand, has faced depreciation pressures due to a lack of US dollars. The CBN has responded by implementing stricter FX policies, making it more difficult for Nigerians to obtain US dollars through traditional channels.

This has pushed many Nigerians towards peer-to-peer (P2P) cryptocurrency marketplaces, where they can buy Bitcoin and Tether (USDT) – a stablecoin pegged to the US dollar – with their Naira. These cryptocurrencies can then be used for international transactions or converted back to Naira at a potentially more favorable rate.

However, the CBN views this rise in crypto adoption with suspicion. In February 2021, the CBN directed all banks and financial institutions to cease facilitating transactions involving cryptocurrency exchanges. This move aimed to curb “illegal” activities associated with cryptocurrencies, but it also effectively cut off a major avenue for Nigerians to acquire and trade crypto.

Despite the ban, Nigerians have found alternative ways to participate in the crypto market. P2P platforms have seen a significant increase in activity, and Nigerians are utilizing offshore exchanges with virtual private networks (VPNs) to access international markets. This has created a cat-and-mouse game between regulators and crypto users, with the CBN struggling to contain the growing popularity of cryptocurrencies.

The situation has left many Nigerians caught in the middle. While they see cryptocurrencies as a potential solution to their economic woes, the CBN’s crackdown creates uncertainty and hinders their ability to participate in the global financial system.

The future remains unclear. The CBN may choose to implement even stricter regulations, potentially mirroring China’s recent crypto ban. Alternatively, they could adopt a more nuanced approach, acknowledging the growing importance of cryptocurrencies and creating a framework for regulated crypto activity.

One thing is certain: Nigerians’ demand for cryptocurrencies is unlikely to wane anytime soon. The country’s economic realities, coupled with the global rise of digital assets, will continue to drive crypto adoption. The question remains: will the CBN adapt and find a way to coexist with this new financial landscape?

Comments are Disabled